What is Spot?

- “Spot” describes a trade struck at the current market price with no future date built in — not necessarily one that settles today.

- In FX and precious metals, a spot trade settles T+2 (two business days later), on a date the market calls the value date.

- The T+2 convention is a 1980s legacy, but it survives because currencies settle in their home countries during non-overlapping banking hours.

- Only in crypto does “spot” mean near-instant (T+0), because the blockchain is itself the settlement system.

- The key distinction is execution versus settlement: you fix your price the moment you deal; when you actually hold the asset depends on the market.

Does a spot trade settle immediately?

Not in FX or metals. The price is fixed instantly, but the currencies or metal change hands two business days later (T+2).

What does “spot” actually mean?

A deal at the current market rate with no future date negotiated into it. The word describes the price and the timing of the decision, not the delivery.

What is the value date?

The day the two sides actually exchange the currencies — T+2 for standard FX spot.

Why still two days in 2026?

Currencies settle through their home countries’ payment systems, which run on non-overlapping local hours. T+2 leaves a wide-enough window for both to be open; holidays push the value date forward.

Does gold have a spot price too?

Yes — the current price per troy ounce for near-immediate delivery, quoted in US dollars. In the London bullion market it also settles T+2, just like FX.

How is crypto different?

Crypto spot settles in close to real time (T+0): the blockchain records and finalizes the transfer itself, with no national banking systems involved.

How big is the spot FX market?

Global FX turnover runs around $9.6 trillion a day (April 2025 survey), with spot about $3 trillion of that.

A quick-read summary of the full article below.

Few words in finance are used as confidently — or as loosely — as “spot.” Traders quote the spot price, exchanges advertise spot markets, and analysts talk about where spot is trading. The word sounds like it should mean “right now, on the dot.” And in one sense it does. But in foreign exchange (FX), the largest market on earth, a spot trade you agree to today doesn’t actually settle for two more business days. Understanding why reveals a great deal about how markets really work beneath the screen.

Where the Word Comes From

“Spot” is short for “on the spot” — an old phrase meaning to act immediately, at the point of decision. Its roots are not in trading floors but in physical marketplaces. For centuries, a farmer who brought grain to a local market sold it then and there: the buyer handed over cash, the seller handed over the sacks, and the deal was done in the same breath. Goods and payment changed hands together. That literal, immediate exchange is the original “spot” transaction.

The term became a formal piece of market vocabulary in the 19th century, as organized commodity exchanges and money markets matured. These markets needed to draw a clear line between two kinds of deal: those settled now (or very nearly now), and those agreed today for delivery weeks, months, or years later. The first became known as spot; the second as forward or futures. The distinction was meaningful then, and it remains the foundation of how markets are organized today.

The Catch: “Spot” Doesn’t Mean Same-Day

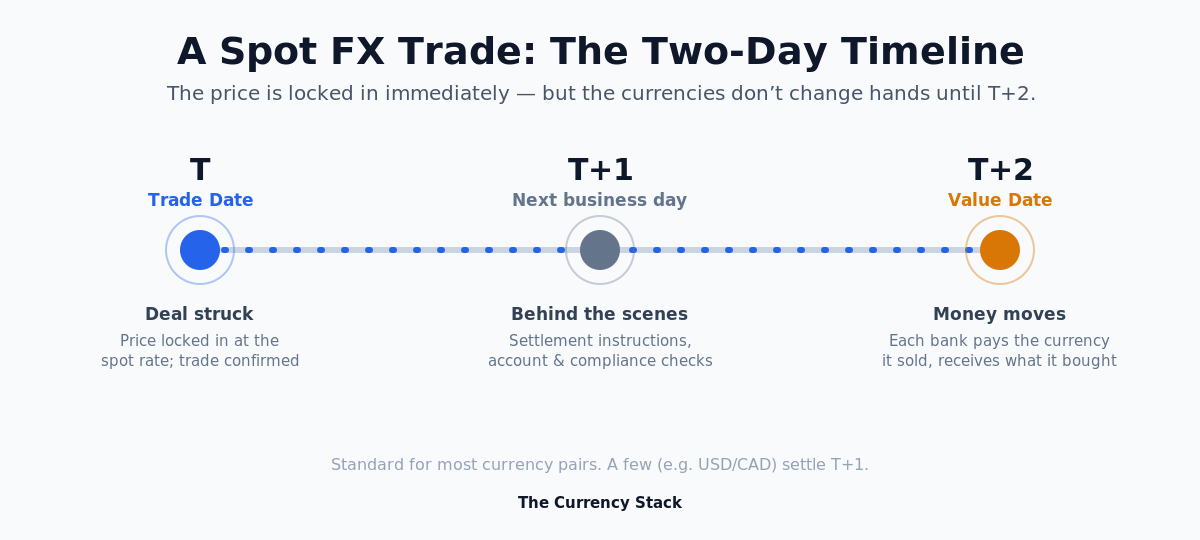

Here is the part that trips up almost everyone. In foreign exchange, a spot trade settles on a T+2 basis — trade date plus two business days. You lock in the price the instant you deal, but the actual currencies don’t change hands until two working days later, a moment the market calls the value date.

So why call it “spot” at all? Because the word describes the price and the timing of the decision, not the timing of the delivery. The trade is “spot” because it is struck at the current market rate, available immediately, with no future date negotiated into the deal. Settlement is simply the plumbing that follows.

To put the scale in perspective: global foreign exchange turnover runs at roughly $9.6 trillion a day (the figure from the most recent industry survey, April 2025), and spot deals account for about $3 trillion of that. It is, by a wide margin, the most liquid corner of the most liquid market in the world — which makes the two-day settlement quirk all the more striking.

The standard timeline for a typical FX spot trade runs like this. On the trade date (T), both parties agree to exchange currencies at the spot rate and the deal is confirmed. On T+1, the back offices prepare settlement instructions, confirm account details, and run their checks. On the value date (T+2), the money actually moves: each bank pays out the currency it sold and receives the currency it bought.

Why Two Days, Even in 2026?

It is tempting to assume T+2 is a relic that fast modern technology should have swept away. The standard did take shape in a slower era — in the 1980s, when capital controls were widespread, the FX market had no central clearinghouse, and back offices still confirmed trades over telex machines. Two days was simply how long it took to confirm details by hand, check accounts, coordinate across institutions, and push payments through correspondent banks. Given the tools of the time, T+2 was a sensible compromise.

Yet T+2 has survived the arrival of instant messaging, real-time payment systems, and blockchain. It persists not out of habit but because of a stubborn structural problem: currencies settle in their home countries, and those countries are not awake at the same time.

Consider a trade between a bank in Sydney and a bank in New York. The Australian dollar leg must settle through Australia’s payment system; the US dollar leg through America’s. But Sydney’s banking day is ending roughly as New York’s is beginning. For both legs to clear, both national payment systems must be open and able to process the transfer — and each runs only during its own local hours, with its own cut-off times. A spot trade is only deliverable on a “good business day,” meaning a day on which the payment systems of every currency involved are open. T+2 provides a window wide enough to accommodate those non-overlapping banking hours. (If a relevant holiday — say, a US dollar clearing holiday — falls inside that window, the value date simply rolls forward another day.)

Layered on top of that are the practical realities of modern banking: smaller institutions still route payments through chains of correspondent banks; settlement systems for different currency pairs remain fragmented and must be reconciled; and every transfer must clear anti-money-laundering, sanctions, and know-your-customer checks before funds can move. None of this is impossible to compress — but compressing it globally, across thousands of institutions and dozens of central banks, is a genuinely hard coordination problem.

The Cost of Waiting Two Days

That two-day gap is not free. Industry estimates suggest that somewhere between $15 billion and $30 billion in capital — and roughly twice as much liquidity — sits tied up in settlement pipes at any given moment, waiting for trades to clear. Capital parked in transit is capital that cannot be put to work elsewhere.

The bigger danger is settlement risk: the chance that you pay away the currency you sold, only for your counterparty to fail before paying you the currency you bought. The longer the gap between dealing and delivery, the more exposed both sides are — and the risk spikes precisely when markets are most stressed. During the extreme volatility of March 2020, margin requirements across the market jumped to roughly 300% of their historical averages, straining institutions exactly when stability mattered most. This is the same hazard that, decades ago, gave the industry its cautionary name for it — Herstatt risk, after a German bank whose 1974 collapse left counterparties unpaid mid-settlement. Much of the modern settlement infrastructure exists to tame it.

Spot in Precious Metals

Gold, silver, platinum, and palladium have a spot price too, and it behaves much like a currency’s. The spot price is the current market price for one troy ounce for near-immediate delivery, quoted in US dollars per ounce, and it serves as the benchmark from which everything else — coins, bars, jewelry, and forward contracts — is priced.

And here the parallel with FX is exact, not approximate. In the London bullion market, the heart of global precious-metals trading, spot metal also settles T+2 — two good business days, with the dollar leg clearing through New York and the same holiday-roll rule applying. So a “spot” purchase of gold is no more same-day than a spot purchase of euros. The price is immediate; the delivery, once again, takes two days. Forward prices for metals are then built on top of this spot price, adjusted for storage, insurance, and financing costs.

Spot in Cryptocurrency

Cryptocurrency is where “spot” finally lives up to its name. Spot trading in crypto means buying or selling the actual coin at its current market price, taking real ownership of it in your wallet — as opposed to crypto futures or derivatives, where you merely speculate on price without ever holding the asset.

Crucially, crypto spot trading settles in something close to real time — effectively T+0. Buy Bitcoin on a spot exchange and, once the network confirms the transaction, the coin lands in your wallet within minutes. There is no two-day wait, for one simple reason: the blockchain is the settlement system. A crypto trade doesn’t need two national banking systems to be open at the same time, because it doesn’t touch them at all. The network itself records and finalizes the transfer. It is the closest thing in modern markets to that original farmer’s exchange — value for value, settled on the spot.

Spot vs. Forward: The Core Distinction

Stepping back, the cleanest way to understand spot is to set it against its opposite. A spot trade is executed at today’s market price for near-term settlement — T+0 in crypto, T+2 in FX and metals — and, because you take delivery, it gives you direct ownership of the asset. A forward or futures trade is also agreed today, but for settlement on a specified future date; it locks in a price for later, often uses leverage, and is typically a bet on where the price will go rather than a transfer of the thing itself. Spot is about owning; forwards are about agreeing now to transact later.

That single distinction — immediate ownership at the current price, versus a dated agreement for the future — is the dividing line that runs through every market, from the wheat pit of the 1800s to a Bitcoin exchange today.

The Bottom Line

“Spot” carries the same meaning everywhere in finance: a trade struck at the current market price, with no future date built into the deal. What it does not reliably mean is “settled today.” In foreign exchange and precious metals, the world’s deepest spot markets, delivery still lands two business days later — a T+2 convention born of 1980s technology but sustained by the unavoidable reality that currencies settle in different countries at different hours. Only in crypto, where the blockchain collapses trading and settlement into a single step, does spot truly mean instant.

The lesson worth carrying away is the gap between execution and settlement. When you deal at spot, you fix your price the moment you click. Whether you actually hold the asset that instant — or two days later — depends entirely on the market you’re in. Knowing the difference is one of the small pieces of literacy that separates someone who simply trades from someone who understands what they’re trading.

Further reading: Bank for International Settlements, “Triennial Central Bank Survey — OTC foreign exchange turnover in April 2025”; LBMA & LPPM, “A Guide to the London Precious Metals Markets.” Previously in this series: What is Money? and Types of Money in a Modern Economy.