Silver, Gold, and the Birth of Exchange

- Three ancient civilizations built the conceptual scaffolding of modern money: the unit of account, the trusted coin, and the paper claim.

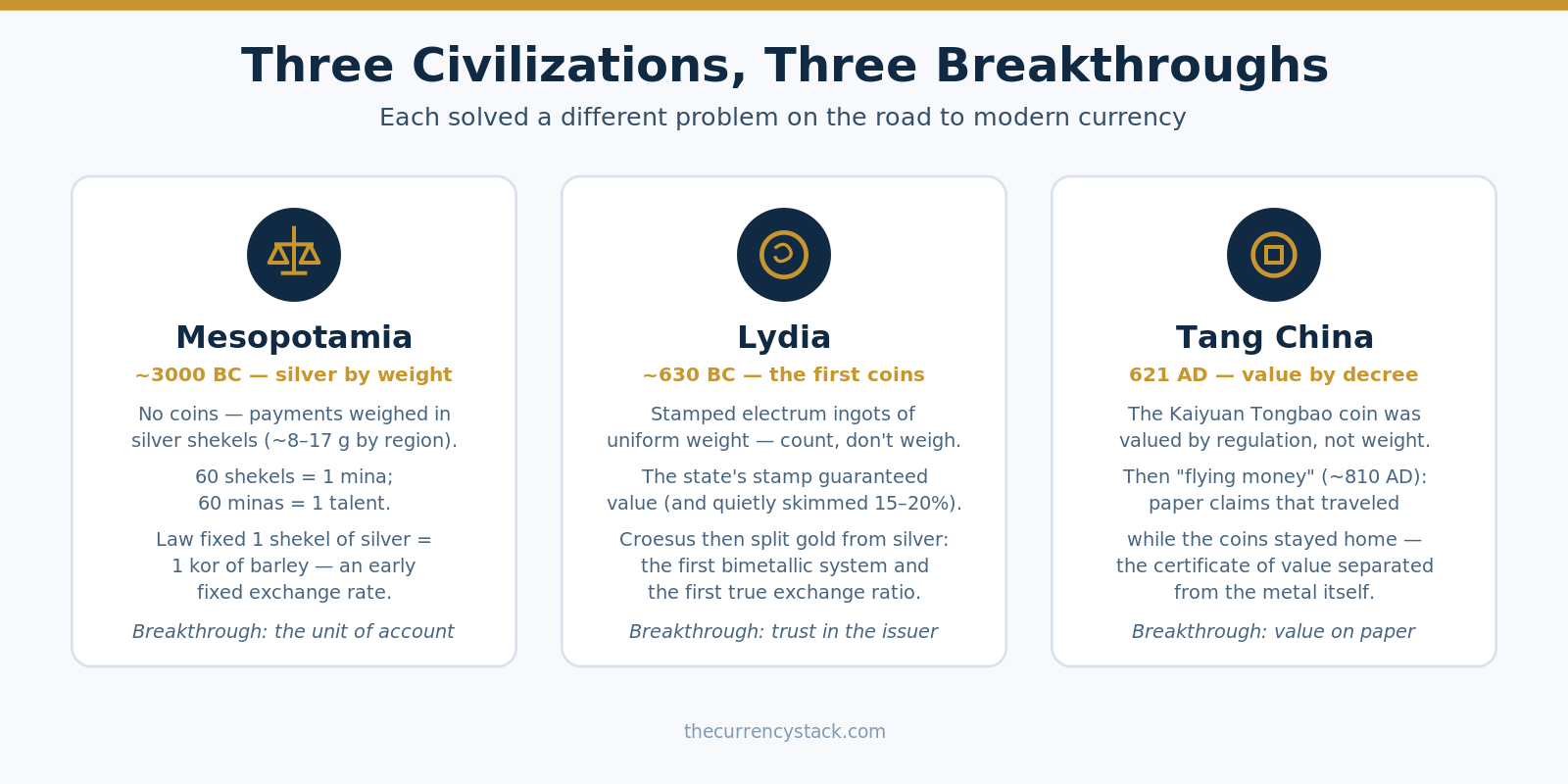

- Mesopotamia used weighed silver as a “money of account” — the shekel began life as a unit of weight — and set history’s first fixed exchange rate, barley to silver.

- Lydia invented coinage (around 630 BCE), moving the guarantee of value from the metal to the issuer’s stamp — and supplied the first case of currency debasement.

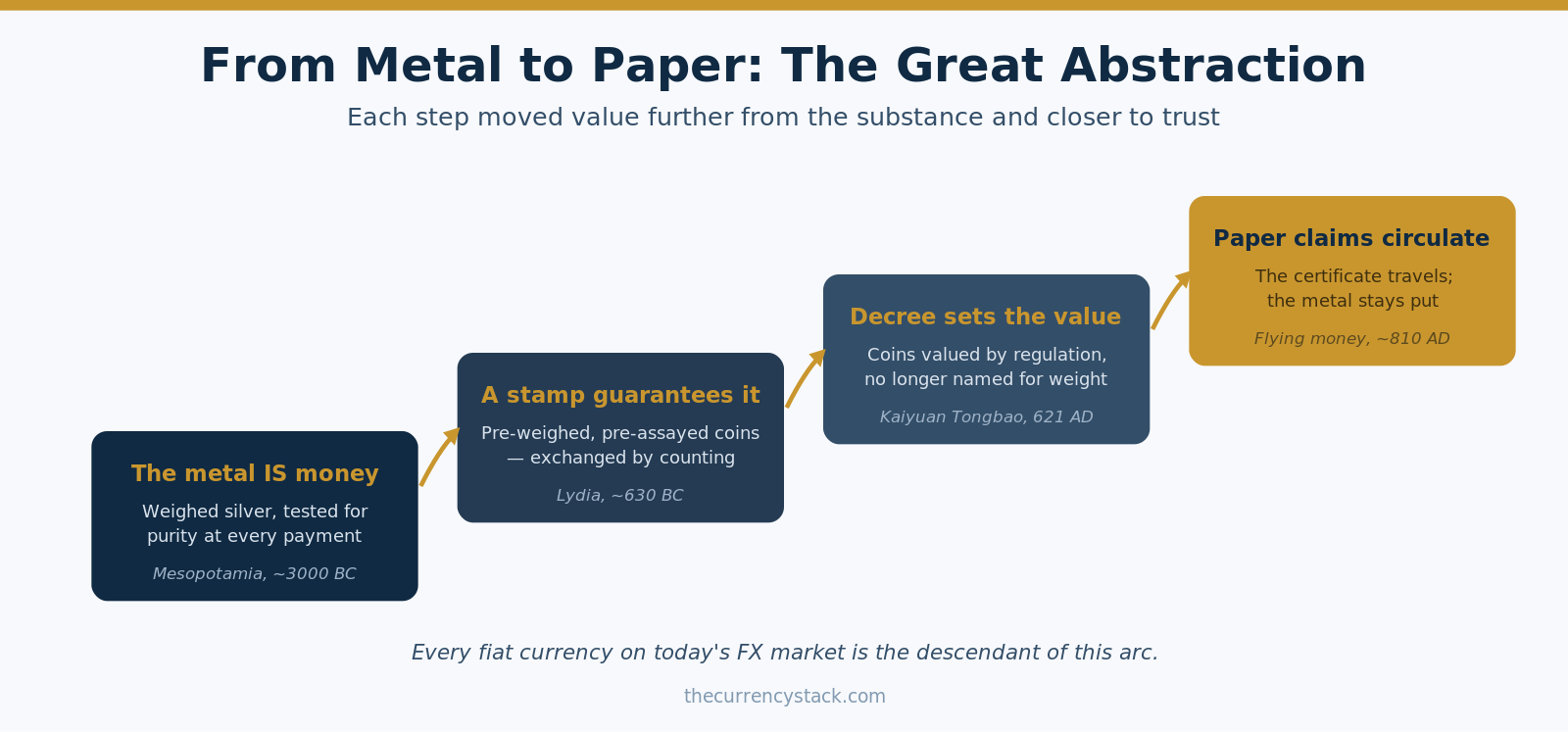

- Tang China abstracted value away from metal entirely: coins valued by decree, then “flying money,” an early transferable paper claim.

- Together they trace a single arc — from intrinsic value to representational value — that underpins every fiat currency and FX quote today.

What did Mesopotamia contribute?

Weighed silver as an abstract unit of account (the shekel, originally a weight), and the first fixed exchange rate — barley pegged to silver in the Laws of Eshnunna.

Why was the Lydian coin such a breakthrough?

It moved the guarantee of value from the metal to the issuer. Pre-weighed, pre-assayed stamped coins could be exchanged by counting instead of weighing — the seed of all trust-based money.

What was the first currency debasement?

Lydia’s royal coins were valued as about 73% gold but quietly debased to around 54%, earning the crown a profit on every payment — the first cautionary tale about issuer power.

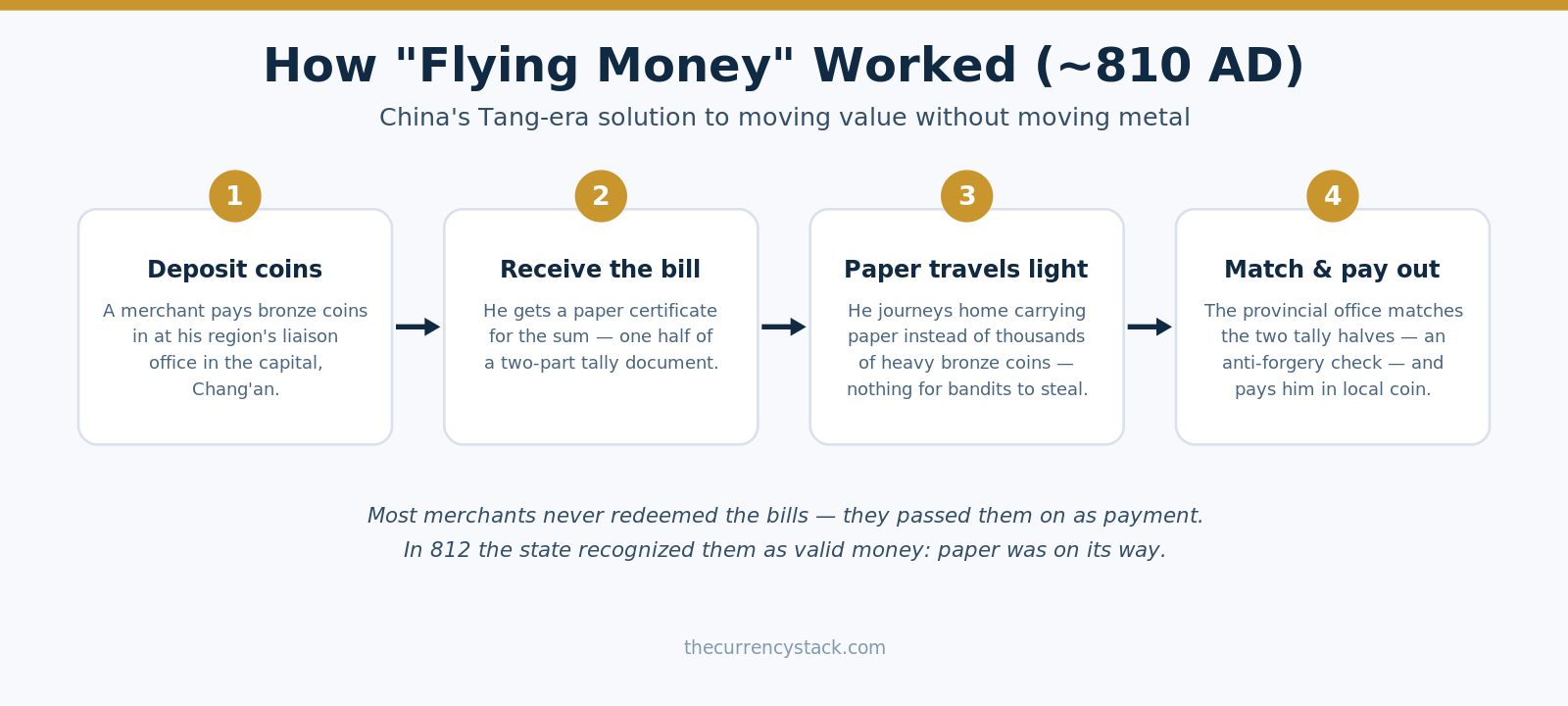

What was “flying money”?

Tang China’s feiqian: a merchant deposited coins in the capital and carried a paper tally home to redeem for local coin. The claim traveled; the metal didn’t.

Was flying money the first paper currency?

No — it was a transferable claim on metal (a bill of exchange). True paper currency came later, with Sichuan’s jiaozi in the 10th–11th century.

Why does ancient money matter to FX today?

The same arc from intrinsic to representational value underpins every fiat currency; ancient bimetallic ratios were the first cross-rates, and trusting a token is still the wager every currency trader makes.

A quick-read summary of the full article below.

Every fiat currency traded on today’s foreign exchange market is the descendant of ideas worked out thousands of years ago — in the grain markets of Mesopotamia, the mints of Lydia, and the treasury offices of Tang China. Between them, these three civilizations built the conceptual scaffolding of modern money: the unit of account, the trusted coin, and the paper claim. This is the story of how value learned to leave the metal behind.

Mesopotamia: Money Before Coins

Long before coins existed, Mesopotamia ran on weighed silver. From roughly 3000 BC, silver became the region’s standard of value alongside barley — prized, portable, and in relatively steady supply. The core unit was the shekel, a word that began life not as money at all but as a weight, from a Semitic root meaning “weighing.” The system scaled in base-60 steps that would have pleased any accountant: 60 shekels to a mina, 60 minas to a talent, with reference weights checked against royal masters.

Two features make Mesopotamia the conceptual starting point of everything that followed. First, silver functioned as money of account: most transactions were settled as standard weights of silver even when no metal physically changed hands. Prices, debts, and wages were expressed in silver as an abstract reference — the original unit of account. Second, the law codes created what may be history’s first fixed exchange rate: the Laws of Eshnunna pegged one kor of barley to one shekel of silver, an administrative parity between two completely different media.

The system’s weakness was distinctly modern too. A shekel was never one universal standard — actual weights ranged from roughly 8 to 17 grams depending on the era and the city — so merchants needed trusted, calibrated weights to transact, an early version of needing a reliable reference rate. And because silver was so valuable, small weighing errors or impure metal meant large losses. Purity and accuracy were everything. Markets fluctuated hard against the administrative pegs: silver-denominated grain prices rose 600–1,400% between the mid-7th and 5th centuries BC.

Lydia: The Coin Solves the Trust Problem

Lydia’s contribution, beginning around 630 BC in western Anatolia, was to solve Mesopotamia’s weighing-and-testing problem by moving the guarantee from the metal to the issuer.

The raw material was electrum, a natural gold-silver alloy panned from the river Pactolus. Electrum had a valuation problem: its gold content varied from nugget to nugget, and checking quality by touchstone streaks was workable for one large lump but hopeless for a bag of small pieces. The Lydian breakthrough was to issue small stamped ingots of uniform weight whose value was set and guaranteed by the authority whose stamp they bore. Pre-weighed and pre-assayed, coins could be exchanged by counting rather than weighing — the seed of all trust-based money since. The discipline was remarkable: the lion-head royal series ran through seven denominations, from a 4.7-gram third-stater down to a 1/96th stater of just 0.15 grams.

Lydia also supplies history’s first cautionary tale about issuer power. The royal coins were officially valued as natural electrum — about 73% gold — while their actual content had been quietly debased to around 54%, yielding the crown a 15–20% profit on every payment. Sovereigns have been tempted by the difference between a currency’s face value and its substance ever since.

Around the mid-6th century BC, King Croesus replaced electrum with separate pure gold and pure silver coins — the Croeseids — once refiners mastered the cementation process for parting the two metals. This was the world’s first bimetallic system, and with it came something recognizably modern: an exchange rate. The Persians, inheriting the system, held their gold-silver mint ratio at 13⅓:1 for roughly two centuries while ratios in the Aegean ran between 10:1 and 14:1. Where official and market ratios diverged, undervalued metal flowed out of circulation — Gresham’s Law and arbitrage pressure, two and a half millennia before anyone named them. The ancient dilemma between a rigid fixed mint ratio and a floating market one anticipates the fixed-versus-floating exchange rate debate that still shapes currency policy today.

Tang China: Value by Decree, Then Value on Paper

China’s path differed in both metal and concept. Its everyday money was base-metal bronze cash, not silver or gold — and its great innovation was abstracting value away from metal entirely.

The first step came in 621 AD, when the Tang emperor Gaozu cast the Kaiyuan Tongbao. Earlier Chinese coins had been named for their weight; this one carried the inscription tong bao — “circulating treasure” — and was valued by government regulation rather than by what it weighed. The standard was strict (an alloy of roughly 83% copper, with private casting punishable by death) and astonishingly durable: the template fixed Chinese coinage for over a thousand years and spread across Japan, Korea, and Vietnam, surviving in use into the early 1940s.

The decisive leap followed in the early 9th century. A copper shortage and bans on moving coins between regions made long-distance trade cumbersome — a wagon-load problem, since meaningful sums meant thousands of heavy coins. The solution, crystallizing under Emperor Xianzong (r. 805–820), was feiqian: “flying money.”

A merchant deposited coins at his province’s liaison office in the capital and received a paper certificate — half of a two-part tally document. Back home, the provincial office matched the two halves (a built-in anti-counterfeiting check) and paid out in local coin. No metal traveled; only the claim did. Because the bills were transferable, most merchants never bothered redeeming them — they simply passed them on as payment. In 812 the state recognized them as a valid means of payment and began issuing its own.

A dating note matters here. Flying money was a claim on metal — a bill of exchange — not yet true paper currency. That came later, with the jiaozi of 10th–11th century Sichuan, covered in our earlier article What is Money?. But the conceptual breakthrough belongs to the Tang: for the first time, the instrument of value and the substance of value were physically separate, held together by nothing but a redemption promise and a verification system.

The Arc That Leads to Your Currency Pair

Put the three stories side by side and a single trajectory emerges. In Mesopotamia, the metal was the money, and every payment meant weighing and testing it. In Lydia, a stamp on the metal guaranteed it, so money could be counted instead of weighed. With the Kaiyuan Tongbao, decree set a coin’s value independent of its weight. And with flying money, the claim finally detached from the metal and circulated on its own.

That is the same arc — from intrinsic value to representational value — that underpins every fiat currency and every forex quote on your screen. Weight and fineness were the original market fundamentals; the bimetallic ratios of the ancient world were the first cross-rates; and a Tang merchant trusting a paper tally was making the same wager a currency trader makes today — that the system standing behind the token will honor it. The West, for what it’s worth, didn’t catch up with the paper part until the 17th century.

Previously in this series: What is Money? · Types of Money in a Modern Economy