Types of Money in a Modern Economy

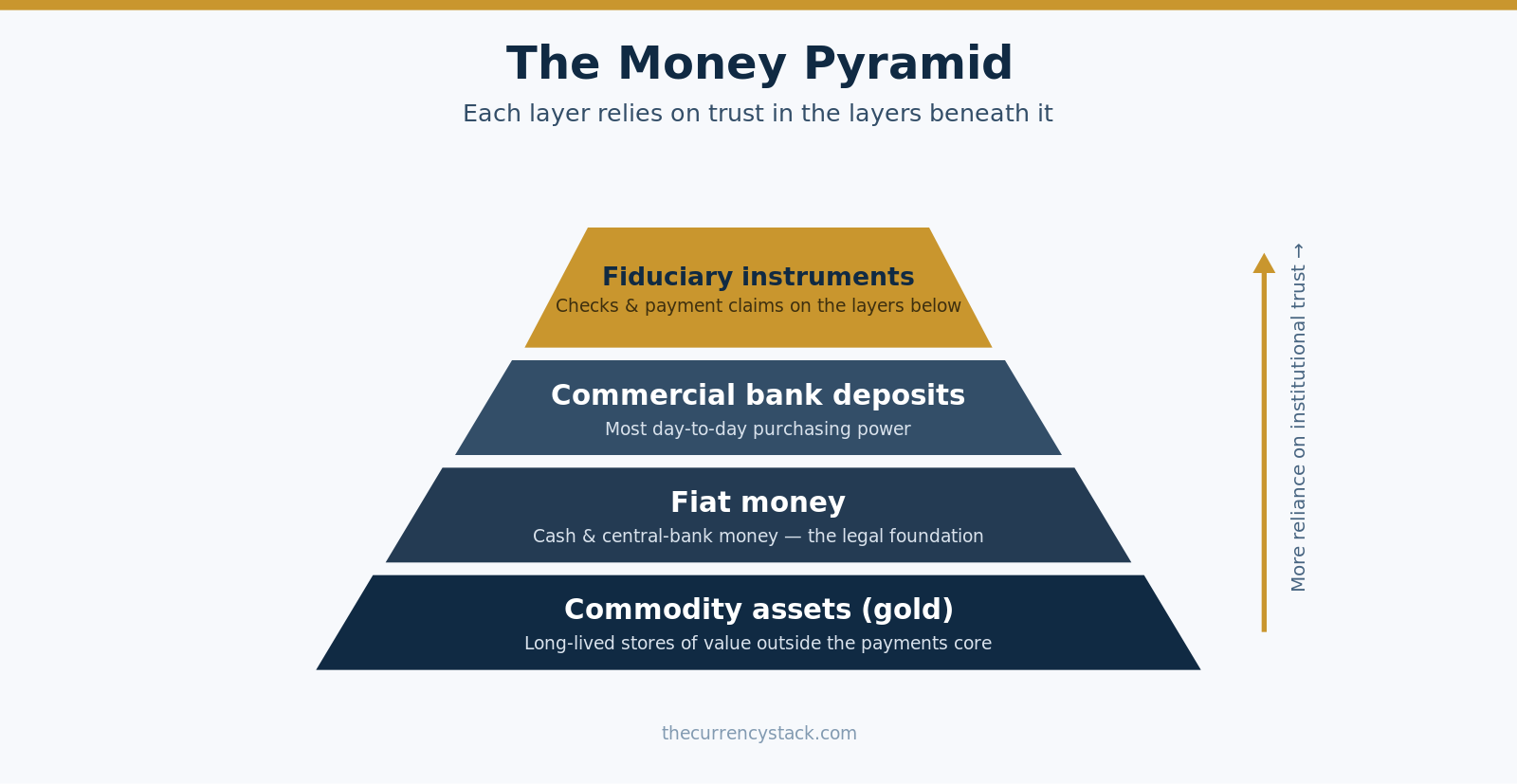

- Modern money exists in several forms at once, layered by how much they depend on trust in institutions.

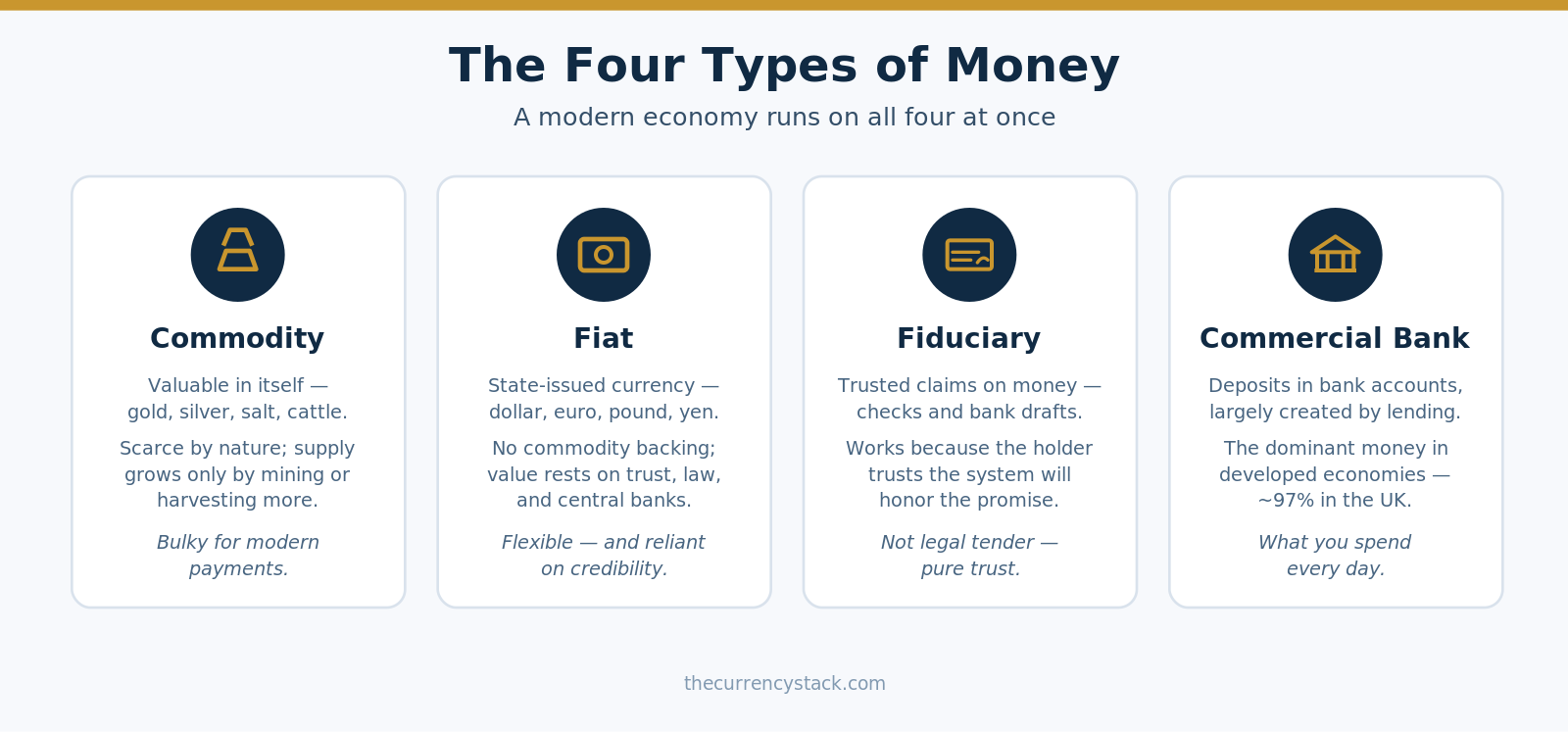

- Commodity money (e.g., gold) has value outside its use as money; fiat money (dollar, euro, pound) rests on government decree and confidence.

- Fiduciary money (checks, drafts) is accepted as a trusted claim on fiat money, but is not legal tender.

- Commercial bank money — deposits, largely created by lending — is the dominant everyday money, roughly 97% of UK money in circulation.

- The forms sit in a hierarchy: the higher the layer, the more it relies on the institutions and counterparties beneath it.

What are the main types of money?

Commodity money, fiat money, fiduciary money, and commercial bank money — coexisting layers rather than stages that replaced one another.

What’s the difference between fiat and commodity money?

Commodity money (gold, silver) has worth in itself; fiat money has worth because a government issues it and people trust and accept it.

What is fiduciary money?

Instruments like checks and bank drafts, accepted because the holder trusts they can be exchanged for fiat money on demand. Unlike fiat, no one is legally required to accept them.

What is commercial bank money?

The deposits in bank accounts — most of it created when banks make loans. It is the money people use daily, and about 97% of UK money in circulation.

How do banks create money?

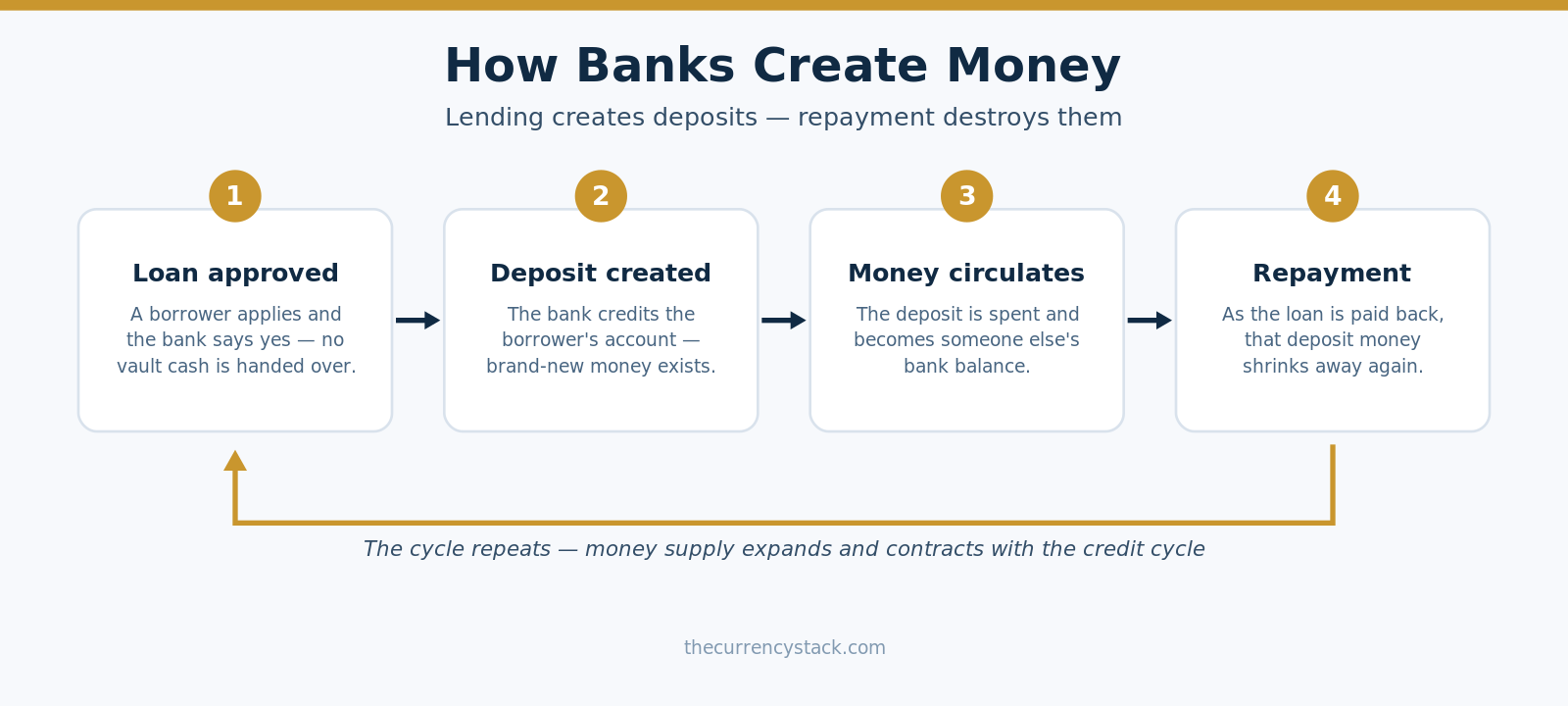

A bank approving a loan credits the borrower’s account with a new deposit rather than lending out existing cash. Repaying loans destroys that money, so it expands and contracts with the credit cycle.

Why does this matter for investors?

Because credit conditions can move markets as powerfully as central-bank announcements, and different assets — gold versus credit-sensitive ones — respond differently to shifts in money and trust.

A quick-read summary of the full article below.

Money looks simple on the surface. People earn it, spend it, save it, and invest it. Yet in a modern economy, money exists in several different forms at once, and each form plays a distinct role in how payments are made, how credit expands, and how the financial system functions.

For investors and curious readers alike, this matters because inflation, liquidity, banking stability, and monetary policy all depend on what kind of money is being created, held, and exchanged. Modern monetary systems are not built on coins and banknotes alone — they are built on layers of trust, legal claims, and bank-created deposits that together make the economy work.

Why Money Comes in Different Forms

As we explored in What is Money?, money performs several jobs at once: medium of exchange, unit of account, and store of value. But no single monetary form performs all of these functions equally well in every setting. Over time, economies evolved from tangible goods with independent value to state-issued currencies and, eventually, to digital bank deposits created through lending.

That evolution reflects a trade-off between physical certainty and economic flexibility. Commodity-based systems offer visible scarcity, while fiat and bank-money systems offer far greater scalability for a large, credit-based economy. The result is a layered monetary structure in which older and newer forms of money coexist rather than fully replacing one another.

Commodity Money

Commodity money is money that has value outside its use as money. Gold and silver are the classic examples, but many societies have also used salt, cattle, and other scarce goods. The key idea is that the asset would still be worth something even if it were no longer used in trade.

This gives commodity money a built-in anchor. Its supply cannot usually be expanded quickly — more of it must be mined, harvested, or otherwise produced — which imposes a natural limit on monetary growth. That scarcity is one reason gold still holds a place in modern portfolios as a store of value and a hedge against monetary instability, even though it no longer serves as day-to-day money in advanced economies.

The drawback is practicality. Commodity money is costly to store, difficult to move in large quantities, and awkward for the volume and speed of transactions a modern financial system requires. Commodity money is like the bricks of a house: real substance and independent worth, but not the easiest material for a fast-moving payments system.

Fiat Money

Fiat money is government-issued currency that is not backed by a physical commodity such as gold. Its value rests on public confidence, legal structures, and the credibility of the institutions that issue and manage it. The US dollar, euro, pound sterling, and yen are all fiat currencies.

What makes fiat money powerful is not intrinsic value but broad acceptance. People use it because taxes are payable in it, debts can be settled with it, and everyone expects others in the economy to accept it. Central banks reinforce that trust by managing inflation, supporting financial stability, and operating the core settlement infrastructure of the monetary system.

Fiat money gives policymakers far more flexibility than commodity money ever could. Because it is not tied to the physical supply of a metal, the central bank can loosen or tighten monetary conditions in response to crises, recessions, or inflationary pressures. But that flexibility cuts both ways: if confidence in institutions weakens or issuance becomes excessive, the purchasing power of fiat money erodes.

A useful analogy: fiat money is a ticket to a trusted venue. The paper or polymer itself isn’t especially valuable, but the ticket works because everyone recognizes the organizer and believes the promise behind it will be honored.

Fiduciary Money

Fiduciary money refers to monetary instruments accepted because people trust they can be exchanged for fiat money on demand. Traditional examples are personal checks and bank drafts, which circulate not because the paper has value, but because the holder expects the banking system to honor the claim.

This category sits between money proper and claims on money. When someone accepts a check, they are really accepting a promise that funds exist and will be transferred when the payment is processed. The term “fiduciary” — from the Latin for trust — captures that reliance on trust, legal enforceability, and institutional reliability. Unlike fiat currency, fiduciary money is not legal tender: nobody is required by law to accept it.

Checks matter less in daily payments than they once did, but the concept survives the technology. Many modern payment instructions still function as trusted claims on money rather than immediate transfers of central bank cash. Fiduciary money is, in practical terms, a written promise between credible parties — it works when the system behind it is trusted.

Commercial Bank Money

Commercial bank money is the dominant form of money in most developed economies. It consists of the deposits held in bank accounts — and a large share of it is created when banks make loans. This is the money most people use every day without noticing it is economically distinct from notes and coins.

When a bank approves a loan, it does not hand over pre-existing cash from a vault. Instead, it credits the borrower’s account with a deposit, creating new bank money that can be spent through the payments system. As the Bank of England puts it: lending creates deposits, and those deposits are money. In the UK, bank deposits make up roughly 97% of the money in circulation; physical cash is only a small fraction.

The process also works in reverse. As loans are repaid, the corresponding deposit money is destroyed, which means bank-created money expands and contracts with the credit cycle. That is one reason credit booms can fuel asset inflation — and why a contraction in lending can tighten financial conditions so abruptly.

Commercial bank money is best thought of as the banking system’s spendable IOUs to the public. They are balance-sheet entries, but because they are widely accepted and redeemable within a trusted system, they function as money in everyday life.

How the Forms Fit Together

These forms of money are best understood as a hierarchy rather than four isolated categories. Commodity assets such as gold sit outside the modern payments core but still matter as stores of value and confidence benchmarks. Fiat money provides the legal and institutional foundation. On top of that sit commercial bank deposits — most day-to-day purchasing power — and above them, payment instruments and claims that depend on trust in the underlying deposits and settlement process.

Thinking in layers explains why trust matters so much: the higher the layer, the more the user relies on the strength of institutions, payment networks, and counterparties standing underneath it.

Why It Matters for Investors

For investors, these distinctions are not academic. Inflation risk, banking stress, credit growth, and policy transmission all become easier to understand once it is clear that modern money is largely created through commercial bank lending rather than existing only as state-issued cash. That insight helps explain why credit conditions can move markets as powerfully as central bank announcements.

It also clarifies why different assets respond differently to monetary shifts. Gold tends to attract attention when confidence in fiat systems weakens, while bank equities, property, and other credit-sensitive assets track the pace of deposit and loan growth. Currency markets, meanwhile, are shaped not just by interest-rate differentials but by trust in the broader institutional framework supporting fiat money itself.

The practical lesson is straightforward: money is not one thing. It is a layered system built from assets, state authority, private credit creation, and trusted claims — and each layer behaves differently under stress. Anyone seeking to understand modern markets, banking, or monetary policy benefits from recognizing those layers clearly.

Further reading: Bank of England, “Money Creation in the Modern Economy” (Quarterly Bulletin, 2014 Q1). Previously in this series: What is Money?